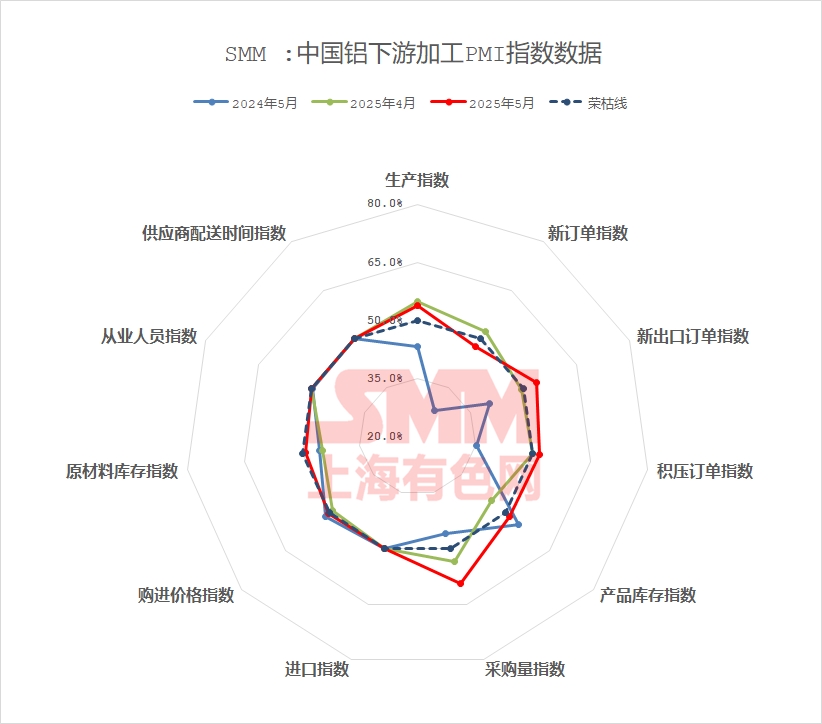

On May 30, 2025:

The composite PMI for the aluminum processing industry in May was recorded at 49.8%, approaching the 50 mark but remaining in contraction territory. It fell by 1.8 percentage points MoM and increased by 8.7% YoY. The main reasons were the arrival of the off-season in May, coupled with the aluminum price fluctuating at highs, weak end-use demand in the industry, and sluggish growth in new orders. By sector, in May, the domestic aluminum plate/sheet and strip industry was affected by weak end-use demand and the seasonal off-season, with both the production index and the new orders index falling below the 50 mark. However, the easing of Sino-US trade tensions spurred a rush in exports for end-use sectors such as home appliances and electronics, boosting production and alleviating the pressure from insufficient domestic demand. The aluminum foil industry contracted overall, with intensified cut-throat competition in processing fees. Enterprises proactively controlled their production pace to cope with the off-season, but high-end products such as battery foil remained relatively stable, supported by the production and sales of new energy vehicles. In May, some construction extrusion enterprises in Shandong, east China, and parts of south China maintained stable production based on orders on hand, but the industry as a whole faced sluggish new orders. Coupled with the continued sluggishness of real estate-related orders and the delayed transmission of the support effect from local governments, there were still doubts about the sustainability of industry demand. In the industrial materials sector, some leading PV frame manufacturers in east China reported that their production had not yet been affected by the 531 period due to their main cooperation with top-tier enterprises, and new orders for June had already been secured, providing support for production this month. However, there were no significant changes in the production of automotive extrusion this month, with new orders being sluggish and orders on hand only sufficient to sustain production until mid-June. Production was expected to remain weak next month. In the aluminum wire and cable sector, despite the delivery of orders as planned by leading aluminum wire and cable enterprises in May, the pace of shipments slowed down. Coupled with the high aluminum prices dampening downstream buying sentiment, procurement was relatively cautious. The primary aluminum alloy industry in May exhibited characteristics of "stability amid pressure and structural transformation," maintaining overall production resilience but with strong wait-and-see sentiment and no rush in exports. The downstream demand for secondary aluminum in May continued the weak trend seen since April, with the off-season characteristics becoming more pronounced. Both domestic and overseas orders showed varying degrees of decline.

Specifically, by product type:

Aluminum plate/sheet and strip: The composite PMI for the domestic aluminum plate/sheet and strip industry in May was recorded at 49.6%, approaching the 50 mark but remaining in contraction territory. Sub-indices showed that the production index (49.3%) and the new orders index (49.3%) were both slightly below 50%, reflecting the impact of weak domestic end-use demand and the seasonal off-season. The new export orders index (62.1%) was significantly higher than the 50 mark, indicating that exports had become the main support. The easing of Sino-US trade tensions spurred a rush in exports for end-use sectors such as home appliances and electronics, boosting production. However, domestic consumption as a whole weakened, with short-term support expected from the 618 sales promotions. In the market, the orderly progress of export orders alleviated some pressure, but overcapacity and insufficient domestic demand led to intensified competition in can stock processing fees. The enterprises' procurement volume index (56.1%) indicated cautious raw material stockpiling. Looking ahead to June, the export recovery is unlikely to offset the deepening off-season, and the PMI is expected to remain in the doldrums, with attention needed on the implementation of infrastructure policies and changes in overseas trade conditions.

Aluminum foil:The composite PMI of China's aluminum foil industry in May registered 47.6%, remaining below the 50 mark, indicating an overall contraction. Sub-indices showed the production index (46.3%) and new orders index (46.3%) weakened simultaneously, reflecting sluggish demand-side growth. The new export orders index (60.7%) provided some support, but the purchasing volume index (47.6%) confirmed weak raw material procurement willingness among enterprises. High-end products like battery foil remained relatively stable, supported by NEV production and sales, while demand for traditional products such as double-zero packaging foil shrank, with intensified cut-throat competition in processing fees. Producers actively controlled production pace to cope with the off-season. Market-wise, eased Sino-US tariffs brought export window benefits, but end-user inventory buildup (e.g., power batteries) and weak domestic demand for air-conditioner foil dampened production enthusiasm. Looking forward, the deepening traditional off-season coupled with uncertainties in overseas order sustainability suggest the PMI will likely maintain a fluctuating and weak trend, with key focus needed on destocking progress in the NEV industry chain and policy support.

Construction extrusion:The composite PMI for construction aluminum extrusion in May dropped back slightly to 53.90%, staying above the 50 mark. Producers with proprietary door and window brands maintained stable production, while some enterprises in Shandong, east China, and south China reported steady May output supported by orders from long-established customers. Some firms with infrastructure orders on hand saw slight production increases, pushing the production index to 70.53% and the procurement volume index to 81.56%. However, enterprises in central China and south China that previously relied on government infrastructure projects reported weak new order growth, compounded by limited local infrastructure projects in Shandong, leading the new orders index to slide to 45.88%. According to the SMM survey, producers generally reported limited engineering orders on hand, with real estate-related orders yet to recover. The industry widely doubts demand sustainability, adopting low raw material inventory strategies due to poor long-term order visibility, keeping the raw material inventory index at 50% in May. Overall, without strong new order support, the construction extrusion PMI in June is expected to stay above the 50 mark but with limited upside room.

Industrial extrusion:The composite PMI for the industrial extrusion sector in May registered 52.23%, barely staying above the 50 mark. Sub-indices showed the production index at 53.45% and new orders index at 54.70%. SMM learned that some PV frame leaders in east China reported uninterrupted production due to collaborations with top-tier enterprises, unaffected by the 531 period, with June orders already secured, supporting May operating rates. However, some small and medium-sized enterprises in Anhui indicated their PV frame orders on hand could only sustain production until mid-June, with no follow-up orders secured by month-end. Although some enterprises in east and south China reported that some OEMs hinted at an upward demand forecast for June, companies believe the actual demand may deviate from projections and are temporarily reluctant to ramp up production. Overall, the industry still faces dual pressures from high aluminum prices and declining processing fees, with most firms maintaining only safety stock levels. The raw material inventory index for this month stood at 46.48%, remaining below the 50 mark. The industrial extrusion sector's PMI is expected to stay in the doldrums in June, and SMM will continue monitoring actual order fulfillment.

Aluminum Wire and Cable: The composite PMI for China's aluminum wire and cable industry in May registered 51, indicating continued expansion. Although top-tier enterprises delivered goods as scheduled, shipment pace slowed, and small and medium-sized enterprises saw reduced production enthusiasm, with the production index at 49.61%. The second batch of ultra-high voltage orders was finalized in May, replenishing orders on hand for leading firms, while new orders for SMEs declined, with the new orders index at 53.38%. The purchasing volume index recorded 43.73%. Despite stable production, persistently high aluminum prices dampened downstream buying sentiment, leading to cautious procurement and further declines in in-plant inventory, with the raw material inventory index at 47.67%. The finished product inventory index was 54.08%, mainly due to slightly slower end-user pick-up pace amid steady production, resulting in a marginal inventory buildup. For June, power grid transmission and transformation orders will provide long-cycle demand support, but new PV installations may weaken, coupled with lackluster infrastructure orders. The aluminum wire and cable PMI is expected to operate below the 50 mark in June 2025.

Primary Aluminum Alloy: The primary aluminum alloy PMI in May was 41.5%, down 4.3 percentage points MoM. The sector exhibited "stable yet pressured, structurally transitioning" characteristics, with production and new orders indices at 36.8% and 31.7%, respectively, reflecting pronounced pressure on domestic demand during the off-season. Leading enterprises' operating rates fluctuated rangebound throughout the month—rebounding slightly early month due to weaker aluminum prices and mid-year full production targets, dipping mid-month amid aluminum price rebounds suppressing processing fees and off-season effects, and stabilizing weakly from late month to month-end. April customs data showed significant export market restructuring: wheel hub exports to the US fell 18.3% MoM to 5,200 mt (first time below 30% share), while Mexico channel exports exceeded 10,000 mt for the first time (up 22.7% MoM and 44% YoY), highlighting top firms' success in mitigating trade risks via overseas capacity deployment. The industry as a whole maintained production resilience but was marked by a strong wait-and-see sentiment. Despite signs of easing in Sino-US trade tensions, enterprises remained cautious in assessing the impact of new tariffs, with no significant "rush to export" phenomenon observed for the time being. Looking ahead, under the dual constraints of off-season factors and uncertainty in tariff negotiations, the industry's operating rates may continue to exhibit a generally stable with slight fall trend. A substantive shift in the trend will await the implementation of details from Sino-US consultations. SMM expects the PMI for the primary aluminum alloy industry to remain below the 50 mark in June, with a high probability of continuing to decline.

Secondary Alloy: In May, the PMI for the secondary aluminum industry declined slightly MoM to 37.0%, continuing to pull back below the 50 mark. Specifically, downstream demand for secondary aluminum in May remained weak, following the trend since April, with the characteristics of the off-season becoming more pronounced. Both domestic and overseas orders showed varying degrees of reduction. Affected by this, secondary aluminum alloy prices were trapped in a dilemma of being "more likely to fall than rise," while the supply of raw materials remained tight and prices stayed high, leading to a further expansion in production losses for enterprises. Influenced by insufficient orders, losses, and the Labour Day holiday, secondary aluminum production in May declined. In terms of inventory, enterprises faced significant sales pressure, leading to a continuous accumulation of finished product inventories. Due to fluctuating aluminum prices and increased difficulty in procuring aluminum scrap, enterprises maintained low levels of raw material inventories. Looking ahead to June, the off-season effect in the secondary aluminum industry will further deepen, and the industry's PMI is expected to remain below the 50 mark.

Brief Commentary:

In May, the aluminum processing industry entered the off-season, with insufficient demand and weak domestic demand affecting most sectors, showing significant structural differentiation. The PMI for the aluminum processing industry in May was recorded at 49.8%, down 1.8 percentage points MoM and up 8.7% YoY, still in contraction territory. The main reasons were the off-season combined with high aluminum prices fluctuating at highs, and weak end-use demand leading to sluggish new orders. By sector: aluminum plate/sheet and strip production and new orders were below the 50 mark, but a rush to export was expected to alleviate domestic demand pressure; aluminum foil experienced an overall intensified contraction, with relatively stable demand for battery foil; some enterprises in the construction extrusion sector maintained stable production, but new orders were weak, and orders related to real estate had not yet recovered; in the industrial materials sector, some leading PV frame extrusion enterprises' operating rates were supported by cooperation with leading companies, but some automotive extrusion orders were only maintained until mid-June; the aluminum wire and cable sector saw an overall slowdown in shipments, with high aluminum prices suppressing downstream procurement; the primary aluminum alloy sector showed stability under pressure, with a strong wait-and-see sentiment overall; the secondary aluminum sector saw a continuous reduction in both domestic and overseas orders, with the characteristics of the off-season becoming more pronounced. Looking ahead to June, disruptions in the overseas trade environment are expected to persist, and domestic end-use demand may remain weak. Under the traditional off-season, this may further suppress production enthusiasm. Continuous attention should be paid to changes in overseas market risks and actual production conditions in various sectors.

》Click to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)